If you have ever scanned your pay stub and spotted GTL on your earnings or deductions codes, then you’re not alone. A lot of workers come across this record and are puzzled, wondering if they are being billed for something and if it even has an impact. As experts, it is highly unlikely that GTL would have a direct effect on your take-home pay, but it can indirectly affect the taxes you owe. Grasping what GTL means, how it is computed, and the reason why it appears on your pay stub will enable you to comprehend your paycheck and prevent surprises when the tax season arrives.

In this blog, we will understand GTL, how it is calculated, and why it shows on your paystub. You can help in making sense of your paycheck stub. Generate detailed and professional pay stubs without the stress by choosing a trusted free pay stub generator.

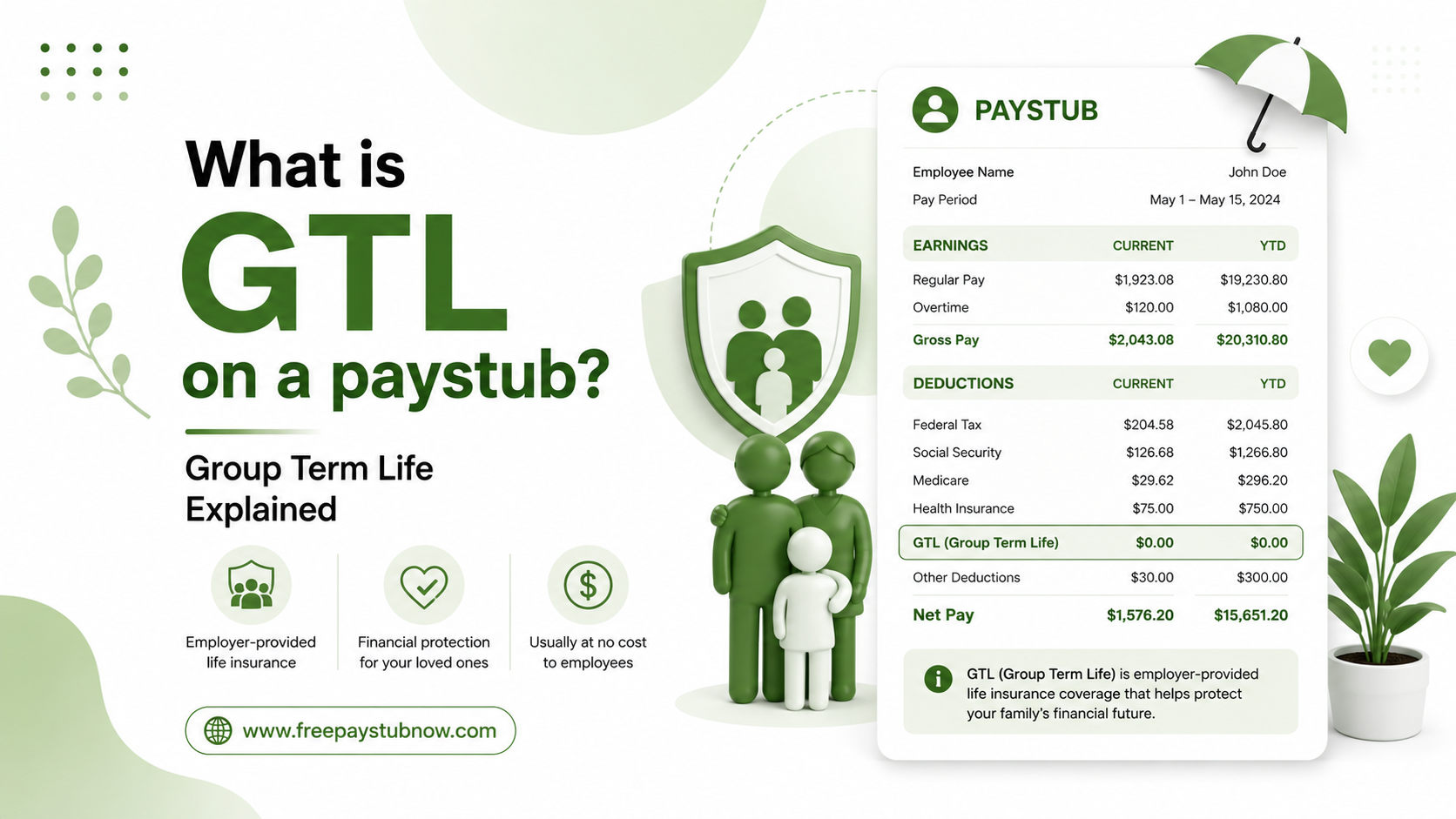

What is Group Term Life Insurance?

Group term life insurance is a type of life insurance coverage provided by an employer, organization, or association to a group of people under a single policy. It offers a death benefit to the insured person’s beneficiaries if the insured dies during the coverage period, typically at little or no cost to the employee.

You won’t receive a larger salary due to GTL. Actually, it’s a phantom amount that the IRS instructs your employer to include in your taxable wages since the life insurance benefit you were given has a value, although that value is never really credited to your account.

Owing to payroll systems, your GTL on paycheck data will boost your gross taxable wages, which in some instances may alter your paycheck deductions (for Social Security and Medicare) slightly, even though your real take-home pay is not decreased by the GTL amount itself in most cases.

What Does GTL Stand For on Paycheck?

GTL stands for “group term life insurance,” which is a type of policy that covers many people, typically employees or group members, under a single policy. In general, the employer or organization owns the policy.

Who is eligible for Group Term Life Insurance?

The eligibility criteria differ by organization and policy; they are typically determined by the following:

- Group membership: Groups could be employees of a certain status, such as high-level executives or members of a labor organization.

- Employment status: Typically, the employee has to be working full-time. However, part-time employees may be eligible if they work enough hours.

- Waiting period: Some employees may have to work at a company for a certain period before they’re eligible to sign up. The waiting period could be a few days to a few months.

- Age: The policy may only be available to people within a certain age range. When the employee reaches a certain age, their coverage may be reduced or canceled.

The $50,000 Rule: Why Does GTL Become Taxable?

Understanding GTL on your pay stub starts mainly with this. IRC section 79 allows a taxpayer to exclude the first $50,000 of group-term life insurance coverage from taxation if such coverage is provided under a policy carried (directly or indirectly) by a taxpayer’s employer. No tax consequences result if the aggregate amount of such policies does not exceed $50,000.

Even so, the calculations change when your coverage is more than $50,000. Income must include the imputed cost for coverage beyond $50,000 based on IRS Premium Table rates and will be subject to Social Security and Medicare taxes. It does not matter if the excess coverage is derived solely from your employer’s base policy or from a combination of your base coverage plus any employer-paid supplemental coverage.

Actually, this $50,000 exclusion threshold is not a recent removal from the tax code but instead a taxed amount that has been a part of the tax code for decades and is still applicable for the current tax year, so employees do not have to track the annual changes to this specific number. What is most important for the calculations is the age-based rate table.

How is GTL’s imputed income calculated?

To calculate the GTL imputed income, use this formula:

[{coverage amount – $50,000) / 1,000] * IRS Monthly Rate * 12 Months.

Example 1:

A 45-year-old with $150,000 coverage has $100,000 excess.

At $0.15 per $1,000 monthly:

$0.15 x 100 x 12 = $180 annual imputed income.

Example 2:

A 55-year-old with $100,000 coverage has $50,000 excess.

At $0.43 per $1,000 monthly:

$50,000 / 1,000 x $0.43 x 12 = $258 annual imputed income.

To verify GLT on the paystub, calculate the following steps:

- Find your coverage amount from HR

- Subtract $50,000

- Divide by 1,000

- Multiply by your age-based monthly rate

- Check your paystub against this calculation

Wondering what GTL is on my pay stub if the amount appears incorrect? The first step is to find out your coverage amount by contacting HR. Besides that, you can know the calculations of W-2 wages from the pay stub to compare with your year-end totals.

Does GTL Affect Your Paycheck or Just Your W-2?

Generally, your net pay (i.e., the real amount credited to your bank account) is not decreased because of GTL imputed income since you do not have to pay any money from your pocket for this benefit. Still, your taxable gross wages on the pay stub will be higher than your regular gross pay only because the GTL amount is added in. This may influence the amounts withheld for Social Security and Medicare taxes on that particular paycheck, as GTL imputed income is subject to FICA.

At the end of the year, all of the cumulative GTL imputed income for the year will be shown in Box 1 (wages), Box 3 (Social Security wages), and Box 5 (Medicare wages) of your W-2, and it is usually also separately identified in Box 12 with the code C. If you have ever wondered why your year-to-date taxable wages differ from your year-to-date gross pay, GTL imputed income is often the cause.

Also Check: YTD Meaning in Paycheck

GTL Insurance Coverage Limits

With any GTL insurance policy, there can be a max death benefit you can select. The maximum benefit is influenced by the following factors:

- Salary: Most commonly, the coverage limit is a multiple of your salary. For example, if you make $100,000 and the limit is three times your annual salary, you can select a death benefit up to $300,000.

- Position: Companies sometimes determine the death benefit maximum based on your position in the company, with more coverage available to higher-level employees

- Flat Amount: The company may set a death benefit maximum, regardless of your salary or position. Otherwise, the limit could be a flat amount, regardless of the employee’s salary or rank within the company.

How is GTL reported on your W-2?

GTL imputed income is printed on your Form W-2 in several places.

To begin with, it is part of your total taxable wages in Boxes 1, 3, and 5. Also, you will find the exact amount of GTL separately in Box 12 under Code C.

So, for taxation purposes, what does GTL refer to on paycheck records? GTL on paycheck records stands for Group Term Life insurance, and the value shown in the line is the taxable part of this benefit. If you want a more thorough explanation of each part, our guide on how to read a W-2 explains what is in each box.

Before you file your taxes, double-check your December paystub to make sure your W-2 details are correct. The year-end GTL on paystubs sum should be the same as the amount in Box 12, Code C.

Additional Group Term Life Insurance Features

While group term life insurance policy details will vary, they may include the following features:

- Accidental Death: There is possibly an accidental death and dismemberment, or AD&D, insurance rider that would provide you with an extra benefit in some situations, like a fatal accident, loss of any two limbs, or loss of both eyes.

- Coverage for Dependents: You may be able to add your spouse or children to the policy as well, although you’d have to pay extra.

- Waiver of Premium Rider: If you become disabled and are unable to work, your premiums will be waived while the policy remains active.

Key Takeaways

Even if you notice GTL on your pay stub, it does not necessarily mean you have done something wrong; it is simply the IRS’s system of making sure that it is employer-provided benefits whose value is kept under control and properly reported at the time of paying taxes (for instance, excess life insurance coverage over $50k).

Having become familiar with the abbreviation GTL as well as the method of calculation will equip you to interpret your pay stub without fear and to refrain from puzzling yourself when you compare your gross pay against the taxable wages shown in your W-2 form. In case the GTL imputed income you have been told of appears to you to be very high, or you are not very clear as to how the insurance coverage you have is arranged, the human resources or payroll section in your place of work is the one that can give you the most correct information.

Frequently Asked Questions

1) What is GTL on a paystub?

On a paystub, GTL stands for “Group Term Life Insurance.” It represents life insurance coverage provided to you by your employer.

2) What is GTL in the salary slip?

“GTL on payroll” stands for “Group Term Life” coverage. This represents an existence coverage policy provided by your organization that covers a collection of employees under an unmarried contract, providing financial security for your beneficiaries in the unfortunate event of your passing away during employment.

3) What does GTL mean for benefits?

Group Term Life (GTL) benefits are corporate-paid benefits that are paid in the event of a worker’s death, even if included. If the overall volume of such policies does not exceed $50,000, there are no tax consequences.

4) What is GTL on the US payroll?

Nowadays, group term life (GTL) insurance is crucial in comprehensive benefits packages because it offers staff an affordable path to coverage without requiring medical tests. Often, simple GTL life insurance is outside the scope of payroll because it’s not considered taxable earnings.

5) Can you cash out group term life insurance?

Because the number of years it covers is limited, it generally costs less than whole life policies. But term life policies typically don’t build cash value. So, you can’t cash out term life insurance.

6) What is the free cover limit in GTL?

The Free Cover Limit (FCL) of coverage in Group Term Life (GTL) is the highest sum assured for insurers without requiring a medical examination or personal health declarations. If the FCL of the policy is ₹50 lakhs, a worker is automatically covered up to ₹50 lakhs; any amount above that requires scientific underwriting.

7) Are group term life insurance benefits taxable?

Group period life coverage is a common place for professional advantage. It generally offers tied or low-fee insurance based on your annual salary. Generally, you lose coverage when you leave your activities, so remember to purchase a policy even when you’re out of work.

8) Does group term life have a cash value?

No, there is no face value for institute lifestyle coverage. Because these miles are a form of term life coverage, these miles can be strictly designed to provide a death benefit for a particular timeframe. It doesn’t serve as a vehicle for saving or investing.

9) What happens if I don’t repay my life insurance loan?

If you default, the loan amount and any accumulated interest could be used to reduce the value of your impairment benefit of greenbacks per dollar. For example, if you have a $250,000 loss of life benefit and still owe $50,000 in life insurance loans, the coverage can be reduced to $200,000.

10) When should I cancel term life insurance?

Cancel term life insurance by self-insuring, which means your dependents are financially sound, the mortgage is being paid off, and your accumulated financial savings or investments can barely cover living and final expenses. Otherwise, loved ones become unprotected in opposition to losing your benefits by dropping insurance.