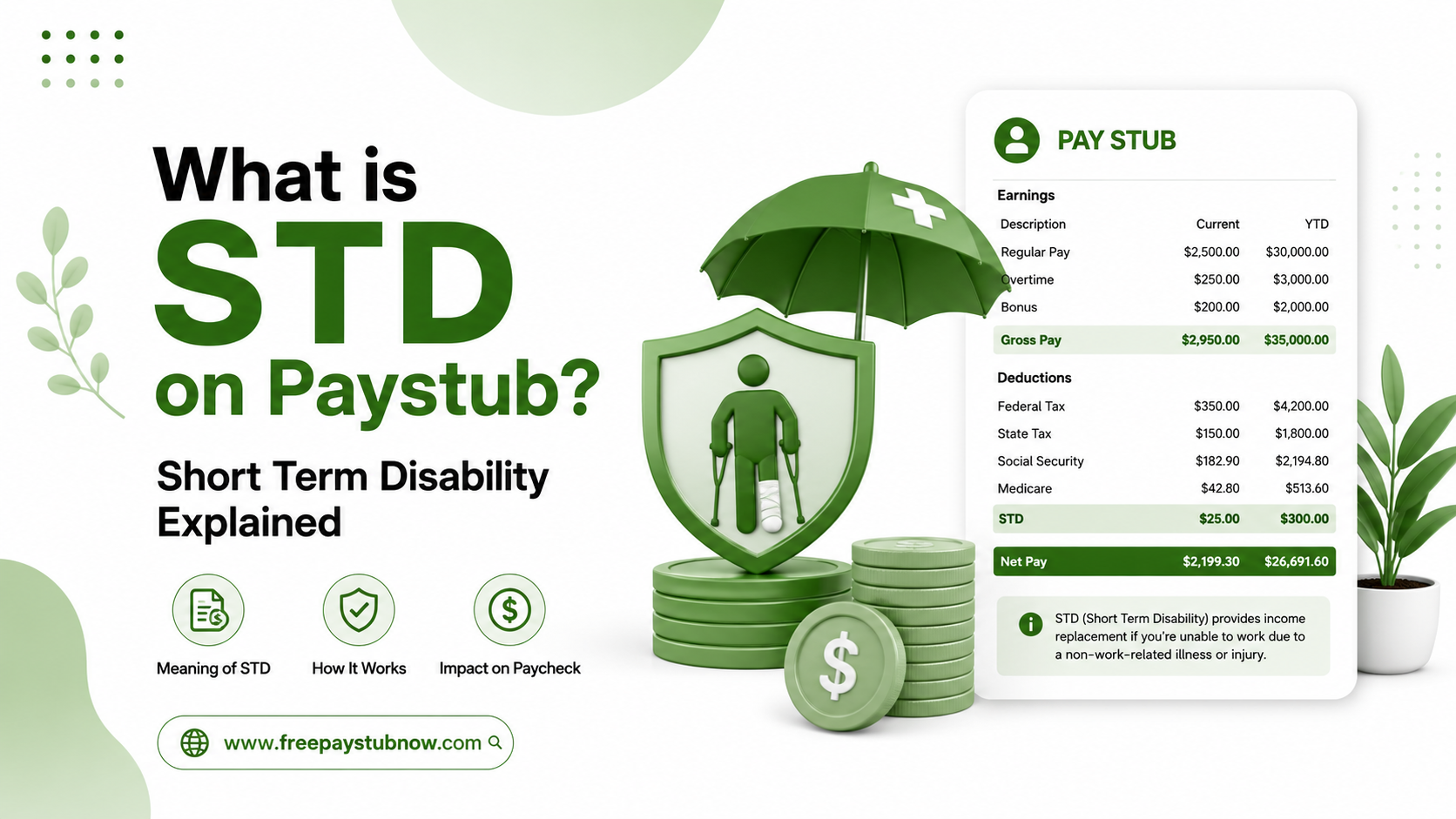

Opening your paystub and spotting a name you don’t recognize is more common than most people think. One abbreviation that trips up a lot of employees is STD. No, it has nothing to do with a medical test at your doctor’s office; on a paystub, STD stands for Short-Term Disability.

If you’ve been searching for what is STD on a paystub means, you’re about to get a straightforward answer, along with everything else you need to know about this deduction.

Using a reliable pay stub generator makes it much easier to see exactly how deductions like STD show up on your earnings statement, and STD is one of the line items employees ask about the most. So let’s break it down in plain English.

STD on Paycheck: The Basic Meaning

When you see STD on a paycheck, it refers to Short-Term Disability insurance.

Employee benefits, which will cover a part of your salary for you if you suddenly lose the ability to work due to circumstances such as an injury, illness, surgery, or a pregnancy-related leave. It has nothing to do with your job, and it just exists to keep you getting a paycheck if something unexpected happens regarding your health.

Think of it as a little financial padding. This type of insurance comes into effect if you are unable to work because of a medical reason, and it pays you part of your normal salary so that you don’t end up with no money for weeks or months on end whilst recovering.

It’s worth pointing out that STD on a paystub is different from workers’ compensation. Workers’ comp covers injuries that happen to an employee on the job. Short-term disability covers everything else: the flu that turns into pneumonia, knee surgery, a difficult pregnancy, or a mental health leave.

Why Does STD Show Up as a Deduction?

Here’s the part that confuses most people: If an STD is a benefit, why is it being taken out of my pay instead of added to it?

The answer is simple. The deduction you see is the premium; basically, the cost of keeping the coverage active. Every pay period, a small amount is pulled from your check to fund the insurance pool. If you ever actually need to file a claim, that’s when the benefit gets paid out to you, separately from your regular paycheck.

So the STD deduction on the paystub you’re seeing now is you paying into the plan, not you receiving money from it.

Pre-Tax vs. Post-Tax STD Deductions

Your STD paycheck deduction will fall into one of two categories:

| Pre-tax deduction | Post-tax deduction |

| The premium is taken out before taxes are calculated. The tradeoff is that if you ever collect a benefit, that payout will usually count as taxable income. | The premium comes out after taxes. In this case, if you ever need to use the benefit, the payout is typically tax-free. |

What Does STD PT Mean on a Paycheck?

If your stub shows STD PT, don’t worry; it’s not a separate program. “STD PT on paycheck” simply means the deduction is being taken on a pre-tax basis. The “PT” is shorthand for pre-tax, so it’s just a more detailed version of the same STD line item, letting you know how the premium interacts with your taxes.

How Much Gets Deducted?

The amount you see for STD on a check stub will usually be one of two things:

- A flat dollar amount taken out each pay period, or

- A small percentage of your gross wages

The exact figure depends entirely on your employer’s insurance carrier and plan design. Some companies cover part or all of the premium as a workplace benefit, while others require employees to pay the full cost through payroll.

If you want to see exactly how a deduction like this will look before it ever hits an employee’s paycheck, previewing a paystub template can help you visualize the layout ahead of time.

When Do Short-Term Disability Benefits Actually Start?

This is where a lot of confusion happens, because paying the premium doesn’t mean the benefit is available immediately.

Most STD plans include a waiting period, usually somewhere between 7 and 14 days, before payments begin. This gap is called the elimination period, and it exists for two reasons:

- To confirm the disability is serious enough to require ongoing leave, rather than a one- or two-day illness.

2. To give enough time for medical documentation and claim paperwork to be reviewed and approved.

During those first days, most employees rely on accrued sick time or paid time off since the disability benefit hasn’t activate yet.

How Long Does Coverage Last?

Once approved, short-term disability benefits generally continue for anywhere from a few weeks up to about six months, though some plans stretch coverage closer to a year. If a medical condition lasts longer than the plan allows, many employees transition into long-term disability (LTD) coverage, which is design to pick up where STD leaves off.

How to Find and Read STD on Your Paystub

If you’re trying to locate this line item yourself, here’s a quick checklist:

- Search for a section called Deductions, Benefits, or Insurance Premiums.

- Look for entries like STD, STD PT, or Short Term Disability.

- Note whether the amount is list as pre-tax or post-tax.

- Cross-check the figure against your benefits handbook or employee portal to confirm the coverage percentage.

If anything still looks unclear, your HR department can pull up the specifics of your plan, including coverage limits and the percentage of wages it replaces.

What is STD on my paycheck?

If you only remember one thing from this article, remember this: what’s STD on my paycheck simply means you’re enroll in and paying premiums toward short-term disability insurance. It is a benefit design to replace part of your income if illness happens to temporarily keep you out of work.

Final Thoughts

Seeing STD on a paystub can be frightening for the first time, but when you learn that it simply stands for “Short-Term Disability,” everything else should make sense. An insignificant amount that silently safeguards your income in the event of an illness.

If you run payroll for your team or need to generate accurate, professional paystubs that clearly reflect deductions like STD, Free Paystub Now makes the process fast and error-free so every employee can see exactly where their money is going, pay period after pay period.

Frequently Asked Questions

1) What does STD mean on a pay stub?

It is short-term disability, a payroll deduction that pays for an insurance benefit to pay part of your wages if you file a claim and end up temporarily unable to work.

2) Is STD the same as sick leave?

No. Sick leave is exhaustes first when employees are waiting for the period and before short-term disability starts. An STD typically requires a doctor to document the condition and a claim; sick leave does not.

3) How much does short-term disability pay?

Most plans replace somewhere between 40% and 70% of your regular base pay while you’re on approved leave, though this varies by employer and insurer.

4) Is the STD deduction mandatory?

Depending on your employer and, in some cases, your state. A few states mandate employers provide short-term disability coverage, while most others have it offered on a voluntary basis with employees opting for participation.

5) Can STDs be use for mental health conditions?

Yes, in many cases. Severe anxiety, depression, or burnout may also qualify if you have a note from your healthcare provider indicating the diagnosis and showing that you need the time off.